How to Lower Commercial Auto Insurance Costs in New York

Lower Commercial Auto Insurance Costs in NY by taking a proactive approach to managing your vehicles, drivers, and insurance coverage....

Workers’ Compensation Cost in NY remains an important consideration for employers budgeting for payroll, insurance, and employee-related expenses in 2026. Workers’ compensation insurance is required for most New York businesses, but the total cost can vary significantly depending on your industry, payroll size, claims history, and employee classifications.

Understanding how workers’ compensation premiums are calculated can help employers make smarter financial decisions and identify opportunities to reduce long-term insurance costs.

In this guide, we’ll explain average workers’ compensation costs in New York, the factors that impact premiums, and practical ways employers can control expenses while remaining compliant.

Workers’ compensation insurance helps cover medical costs, lost wages, and rehabilitation expenses for employees who experience work-related injuries or illnesses. In New York, most employers are legally required to maintain coverage under the New York Workers’ Compensation Board requirements.

Coverage requirements generally apply to:

Failure to carry proper workers’ compensation coverage may result in fines, penalties, or stop-work orders.

Workers’ compensation insurance premiums in New York are commonly calculated using the following formula:

Payroll × Classification Rate × Experience Modifier (EMOD)

Insurance carriers typically calculate rates per $100 of payroll.

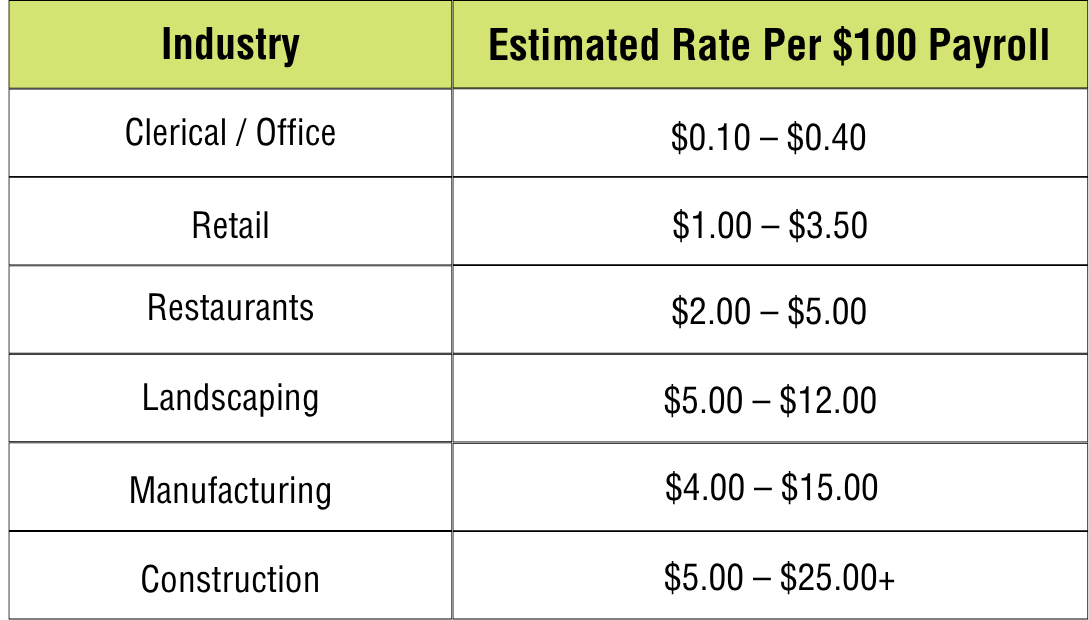

Businesses operating in higher-risk industries—such as construction or manufacturing—often pay significantly higher premiums due to increased injury exposure.

Workers’ compensation rates are largely determined by employee job classifications.

Higher-risk positions typically generate higher premiums. For example, office employees generally have lower rates, while roofing or heavy construction workers often have much higher premiums.

Proper classification is essential because misclassifying employees can increase costs unnecessarily.

Premiums are directly tied to payroll size. Larger payrolls generally result in higher workers’ compensation costs.

For example, a company with $100,000 in payroll may have much lower premiums than a business with several million dollars in annual payroll.

Employers should regularly review payroll estimates to avoid unexpected audit adjustments.

The experience modification factor, commonly called EMOD, reflects your company’s claims history compared to similar businesses.

Employers with strong safety records and fewer claims often benefit from reduced insurance costs.

Insurance carriers carefully evaluate prior workplace injuries and claims frequency.

Businesses with:

may face higher premiums over time.

A proactive workplace safety strategy can help improve claims outcomes and lower long-term costs.

Many insurance carriers reward employers that invest in workplace safety initiatives.

Examples include:

Improved workplace safety may help reduce claims and improve EMOD scores over time.

Several factors are influencing workers’ compensation cost trends in New York during 2026.

Some employers may experience lower premiums due to improved claims management, competitive insurance markets, enhanced fraud prevention efforts, and updated rate adjustments.

However, high-risk industries may still experience elevated costs depending on payroll growth and injury exposure.

Incorrect classifications are one of the most common causes of inflated premiums.

Employers should periodically review:

Reducing workplace injuries is one of the most effective ways to lower insurance costs over time.

Consider implementing:

Fast reporting and proactive claims handling can help reduce claim severity and duration.

Employers should establish procedures for:

Many employers renew policies without reviewing classifications or comparing pricing.

An annual review can help identify incorrect payroll estimates, outdated classifications, and cost-saving opportunities.

Employers should also understand the compliance risks tied to workers’ compensation policies, audits, and claims management. Bene-Care’s previous blog post Workers’ Compensation: Avoiding the Most Common Mistakes, highlights several issues New York businesses should avoid to help reduce penalties and unexpected costs.

Yes. Most New York employers are legally required to carry workers’ compensation insurance.

Businesses without proper coverage may face:

Employers should review state requirements carefully to ensure ongoing compliance.

Understanding the workers’ compensation cost in NY can help employers budget more effectively and identify opportunities to reduce insurance expenses.

Although pricing varies by industry and claims history, businesses can often control costs through:

As insurance regulations and market conditions continue evolving in 2026, employers that actively manage risk and compliance may be better positioned to control long-term workers’ compensation expenses.

Employers looking to better manage risk and reduce long-term insurance expenses may benefit from exploring Bene-Care’s commercial insurance options.

If your organization needs support with payroll, HR, compliance, or workforce management strategies, contact Bene-Care’s team to learn how we can help simplify employer operations and support business growth.